Affordable 401(k) Retirement Plans for Small Business Owners

Help your employees achieve their retirement goals while putting tax savings in your company’s pocket.

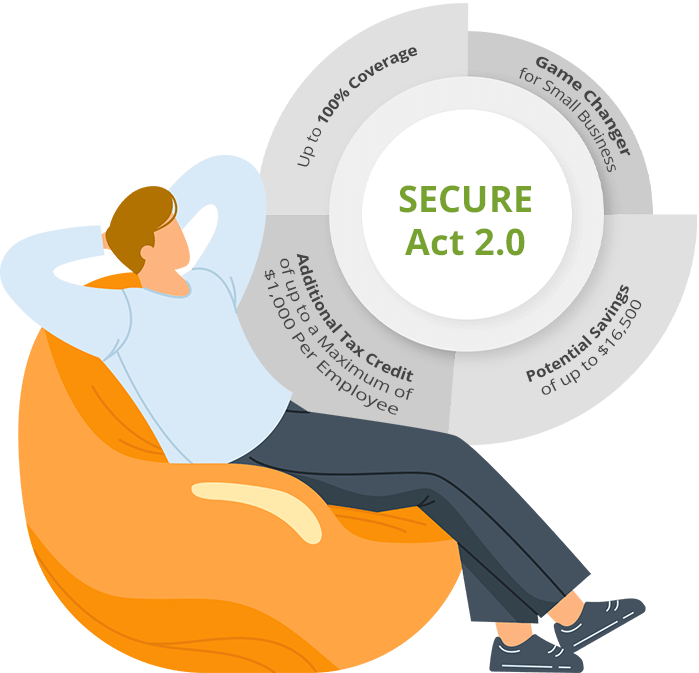

SECURE Act 2.0 is a Game-Changer for Small Business Retirement Plans

Don’t miss out on these benefits:

- Up to 100% coverage of 401(k) retirement plan start-up costs for qualifying businesses – a potential savings of up to $16,500.1

- Eligible businesses that choose to give matching or profit-sharing contributions to their employee retirement plan may qualify for an additional tax credit of up to $1,000 per employee. 2

See If You Qualify.

Backed by the support and experience of the nation’s largest 401(k) plan provider3.

Support your employees in building their future when you start a 401(k) for small business.

SurePayroll, a Paychex® company, can guide you in setting up a 401(k) built for you.

Our competitively priced, quality 401(k) retirement plan can help you retain employees and improve satisfaction. Set up a 401(k) plan for your employees with SurePayroll today.

- Competitive and transparent fees built for a small business budget

- Flexible: Choose from pre-selected investment menu available through Mesirow, our fiduciary partner; or create your own investment line-up from 1,600 investment options

- Ease of use with one trusted source for 401(k) retirement plans and payroll–one platform, one provider

- Plan administration support, so you can focus on your business

- Leverage the benefit of a 401(k) to attract and retain employees

- Access your small business 401(k) plan anytime, anywhere with mobile app and online platform

Call 866-497-2028 to learn more about small business 401(k) plans.

Are You Ready for State-Mandated Retirement Plans?

Every state is different when it comes to retirement plan mandates. If you have employees working in different states, you may need to consider each state’s requirements.

Not all retirement plans are created equal. A 401(k) plan from a provider like SurePayroll may be a better way to save for both you and your employees. A state-facilitated IRA has lower employee contribution limits, more administration demands, and is not eligible for SECURE Act 2.0 small business 401(k) tax credits.

Find out what your state requires.

Watch our webinar to discover if your business qualifies for the $1,000 employer contribution tax credit per employee - Safe Harbor 401(k) Webinar

Affordable 401(k) Plans for Small Business

Whether you have one employee or many, SurePayroll can guide you in finding the right retirement plan for your small business.

Comparison of Common Small Business Retirement Plans

| Sure401k | |||

| Feature | Traditional 401(k) | Safe Harbor 401(k) | Simple IRA |

| Basic Plan Type | Defined contribution | Defined contribution | IRA based |

| Who Can Contribute | Employee; employer contributions are optional | Employee and employer | Employee and employer |

| Employee Contributions |

|

|

|

| Roth Contributions | Yes, within deferral limit | Yes, within deferral limit | No |

| Employee Contributions | Employer contributions are optional |

or

|

or

|

| Profit Sharing | Yes | Yes | No |

| Maximum Annual Contribution Per Participant * Maximum compensation limit is $330,000 in 2023 |

Employer / Employee Combined: Up to the lesser of 100% of compensation or $66,000 ($73,500 age 50 and older) |

Employer / Employee Combined: Up to the lesser of 100% of compensation or $66,000 ($73,500 age 50 and older) |

Employee: $15,500 (if 50 years or older, an additional $3,500 allowed) Employer: Must make matching contributions up to 3% of employee compensation or contribute 2% of total eligible employee compensation* |

| Employee Eligibility Note: For all plan types, the plan sponsor may exclude union employees |

Employers can select any of the following participant eligibility requirements:

|

Employers can select any of the following participant eligibility requirements:

|

Participants must:

and

|

| Minimum Vesting | Immediate on employee contributions; Employer contributions can be subject to vesting schedule | Immediate on employee and most safe harbor contributions; Employer contributions can be subject to vesting schedule | Immediate |

The Importance of Offering a Retirement Plan

A large percentage of Americans are not building up sufficient assets needed to maintain their standard of living in retirement. The problem is getting worse for younger generations.

About 25% of non-retired adults in the U.S. do not have any retirement savings.4

The median of total household retirement savings among all workers in 2020.5

Social Security is projected to run out of funds in 13 years. At present, the Social Security Trust Fund is funded through 2034.6

94% of employees are interested in a 401(k) plan, second only to health insurance.7

The small businesses who don’t offer employee retirement plans cite expense, administrative burden, and confusion about how to choose a provider.

Small Business Retirement Plans FAQs

What Are Retirement Services?

Retirement services cover the full range of services needed over a plan’s life, particularly for a business or organization managing multiple plans. These can include plan design, investment, conversion, setup, enrollment, administration, and compliance testing.

Can A Small Business Have a 401(k)?

Yes, a small business can have a 401(k). Offering a 401(k) retirement plan is a great way for small businesses to attract and retain talent.

How Many Employees Do You Need to Offer 401(k)?

Small businesses with one employee to many can offer 401(k) retirement plans. SurePayroll is great for companies with one employee to 100.

What is a 401(k) Retirement Plan?

A 401(k) retirement plan is a type of retirement account that allows employees to contribute a defined amount of pretax or Roth (after tax) dollars each pay period. Employers also can match part or all the employee's tax-deferred retirement contributions, or provide a profit-sharing contribution, although those contributions are not required. A 401(k) plan is a great option for entrepreneurs and small businesses, particularly since pension plans are no longer common and the future of Social Security benefits is unpredictable.

Start saving with Sure401k® now and contact a small business retirement plan specialist at 866-497-2028.

What Are the Most Common Retirement Plans?

Employers most commonly use 401(k) plans because of their flexible plan designs and the ability to save much more than other retirement plans such as IRAs.

What Are the Different Types of 401(k) Plans?

Sure401k® offers popular 401(k) plan options at affordable prices so you and your employees save as much as possible.

Traditional 401(k) plan allows employees to save for their retirement through payroll-deducted contributions while providing employers the option to make additional contributions to their employees' 401(k) retirement accounts. However, due to required annual non-discrimination testing—developed to ensure 401(k) plans do not favor owners or highly compensated employees (HCE) more than other employees—HCEs and business owners may have limits imposed on their annual contribution amounts.

Safe Harbor 401(k) plans provide the same features as a traditional 401(k) plan and bypasses annual non-discrimination testing. A Safe Harbor plan requires minimum annual employer contributions using either a matching formula or a fixed 3% annual contribution.

Solo(k) gives owner-only and family-only businesses the ability to make the maximum allowable contributions to a small business retirement plan while providing access to accumulated balances through a loan feature. Business owners and their spouses receive the same advantages of a traditional 401(k) plan, including pre-tax and Roth contributions, and higher annual contribution limits than allowed in a SEP-IRA or SIMPLE plan.

There are pros and cons to each type of plan. Businesses tend to use 401(k) plans because they are flexible and enable employees to save more. A small business retirement plan specialist can review the different plan descriptions and help you decide which one is best for your business. Contact us today at 866-497-2028 today.

What Are Typical 401(k) Management Fees?

Some typical 401(k) management fees are:

- Plan administration fees: Day-to-day operational expenses for plan recordkeeping, accounting, legal, trustee services, etc.

- Investment fees: Expenses for 401(k) investment management and other investment-related retirement plan services.

- Individual service fees: Expenses charged separately to the accounts of participants who choose to take advantage of a particular plan feature, such as taking out a plan loan.

Who Uses SurePayroll for 401(k) Retirement Plans?

Small businesses with employees from one to 100 trust SurePayroll to help them deliver 401(k) benefits to their employees. We can help you find the right retirement plan services that not only fit your business, but also help you build and retain a high-quality workforce.

What Type of 401(k) Plan Employee Contributions and Deferrals are Available?

All employees, including small business owners, may defer up to $22,500 per year (or $30,000 per year, if age 50 or older) based on 2023 limits. You’ll find that Sure401k® offers deferral 401(k) plan options so your employees can build their retirement savings.

Pre-tax Deferral is a contribution that is made from gross pay prior to tax deductions. The contributions grow tax-free. The accumulated 401(k) plan balance is taxed upon distribution at the individual's then-current income tax rate.

Roth Deferral is a contribution made on an after-tax basis. These 401(k) retirement plan contributions also grow tax-free, but the accumulated balance is not taxed upon distribution so long as the Roth contributions have been in the plan for at least the past five plan years, and it’s a qualified distribution. If those criteria are met, both the contributions and earnings on the Roth 401(k) plan contribution are tax-free when withdrawn.

Catch-Up Contributions are optional for individuals aged 50 or older so they may defer up to an additional $7,500 to their 401(k) retirement account, for a total allowable deferral of $30,000 in 2023.

Explore your 401(k) retirement plan deferral options now and contact a small business retirement plan specialist at 866-497-2028.

What are Employer Contribution Options?

Small business owners can easily make contributions to their employees' 401(k) accounts with a variety of simple options.

Fixed Company Match enables you to match employees’ 401(k) plan contributions at a fixed rate for a simple, predictable way to help them grow their retirement funds. This option is the most popular matching method for small businesses.

Discretionary Company Match allows you to match a percentage of each employee's deferral, giving the freedom to offer, raise or lower the match percentage annually.

Discretionary Profit Sharing lets you make one-time or periodic contributions to employees' 401(k) accounts, even if they're not actively contributing themselves. We'll prepare estimated profit-sharing calculations upon your request.

For all 401(k) plans, the maximum contribution in 2023 for any one person is limited by law to the lesser of $66,000 or 100% of compensation. If someone is making the full catch-up contribution, the limit increases to $73,500.

How Does a Small Business Set Up a 401(k)?

A small business interested in setting up a 401(k) retirement plan can get started with a simple 15-to-20-minute meeting with a SurePayroll retirement plan specialist. This will help you determine which type of 401(k) retirement plan is the best fit for you and your business. From there, we can set up the 401(k) retirement plan for your business in less than 15 minutes.

Can an LLC Have a 401(k) Plan?

Yes, an LLC can have a 401(k) retirement plan. Any type of business can start a 401(k) plan, including corporations, partnerships, sole proprietors, and LLCs.

Benefits and HR Services

1 Setting Every Community Up for Retirement Act of 2019. New plans may be eligible for up to $5,000 a year over three years and an auto-enrollment credit of $500 a year over three years, for a total tax credit of up to $16,500

2 SECURE Act 2.0. The employer contribution credit is generally a percentage of the amount contributed by the employer, up to $1,000 per employee. This additional credit is limited to employers with 50 or fewer employees and reduced for employers with between 51 and 100 employees. The credit phases out over 5 years.

3 By number of plans in the U.S., PLANSPONSOR Recordkeeping Survey, 2022. Based on results for Paychex. SurePayroll is a wholly-owned subsidiary of Paychex.

5 Non-Profit Transamerica Center for Retirement Studies; 21st Annual Transamerica Retirement Survey of Workers; August 2021 – Usage rights on file

6 https://www.ssa.gov/news/press/releases/2022/#6-2022-1

7 2020 Small Business Employee Study December 2020; A joint study conducted by ClearlyRated and Paychex

8 December 2022 Small Business Retirement: Investing in Your Future, by SCORE. – Usage rights on file.

Health insurance sold and serviced by Paychex Insurance Agency, Inc., 225 Kenneth Drive, Rochester, NY 14623. CA License #0C28207.

Property and casualty insurance products and services are provided by CoverWallet, Inc., an Aon Company and a licensed insurance producer in all states; in CA, CWallet Insurance Services (CA 0K84318). Paychex Insurance Agency, Inc. (PIA) with offices at 225 Kenneth Drive, Rochester, NY 14623, is a licensed insurance agency in all 50 states (CA #0C28207). PIA partners with, and shares compensation with CoverWallet, an Aon Company. ba